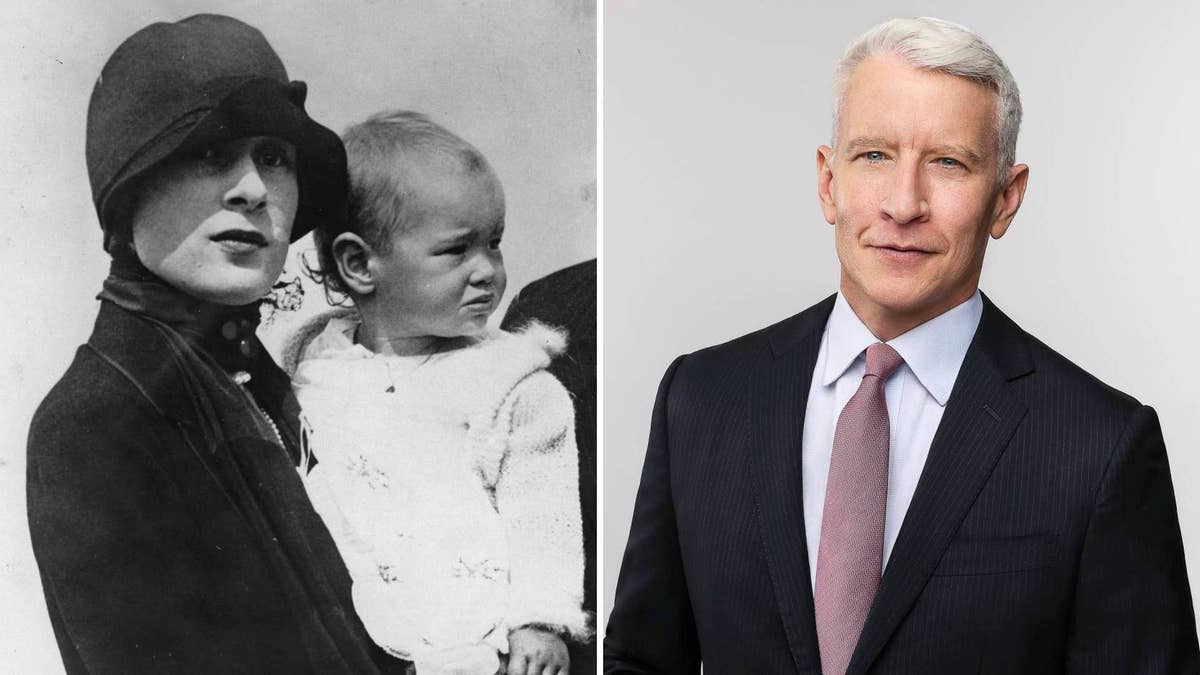

Though he’s the son of late heiress and 1980s denim designer Gloria Vanderbilt, once known as the “Poor Little Rich Girl,” Anderson Cooper doesn’t believe in trust funds or inheritances.

This stance isn’t in spite of his family history, but because of it: his great-great-great-grandfather, Cornelius “the Commodore” Vanderbilt, a billionaire many times over by today’s standards, once held a fortune larger than the entire United States Treasury of the time. In fact, when he died in 1877 at the age of 82, the Commodore had an estimated net worth of $105 million — that’s approximately $3 billion today, or upwards of $150 billion when measured by relative economic power.

By all reports, the industrialist and father of 13, who made his fortune in shipping and railroads, planned to pass it all down to his heirs. According to a family history written by Vanderbilt descendant Arthur T. Vanderbilt II, Fortune’s Children: The Fall of the House of Vanderbilt, the Commodore is said to have told his son William Henry “Billy” Vanderbilt: “Any fool can make a fortune; it takes a man of brains to hold onto it.”

Perhaps ironically, given this foreshadowing, his descendant, CNN icon Cooper, inherited less than $1.5 million from his own mother, with just part of that, if any, being from the Vanderbilt estate, which had been diluted over the years. But is that loss of wealth such a bad thing? Some Vanderbilt descendants — including Cooper himself — would say no.

“From the time I was growing up, if I felt there was some pot of gold waiting for me, I don’t know that I would have been so motivated,” the veteran news anchor emphasized in a 2014 interview on The Howard Stern Show.

© Getty Images

© Getty ImagesAnderson Cooper calls inherited wealth an ‘initiative sucker’

Cooper, who shares sons Wyatt, six, and Sebastian, four, with ex Benjamin Maisani, has all the reason to be wary of trust funds, his family having failed to uphold some core pillars of making a trust work. During the 2014 appearance on The Howard Stern Show, Cooper illuminated his stance on inheritances and trust funds, noting that he had neither. “I think it’s an initiative sucker,” Cooper said of inherited wealth. “I think it’s a curse.”

The silver-haired scion wasn’t the first, however, to express the paradoxical point of view.

More than 100 years earlier, according to Fortune’s Children, Cooper’s great-great uncle William Kissam Vanderbilt remarked: “Inherited wealth is a real handicap to happiness… It has left me with nothing to hope for, with nothing definite to seek or strive for.”

William’s worry would become less of a problem sooner than expected, as the Vanderbilt fortune rapidly dwindled in the blink of an eye.

© Getty Images

© Getty Images © Getty Images

© Getty ImagesThe rapid decline of the Vanderbilt fortune

The Commodore was once widely considered the richest person in the world. However, three generations later, Cornelius’ great-grandson, Cooper’s grandfather Reginald Claypoole Vanderbilt, had seen much of the family wealth slip away.

The family’s fortune largely came to an end with Reginald, who spent much of his 45 years on Earth spending; in 1925, he ended up dying in debt, aged 45. Per a 1932 New York Times report, he left behind an estate of just $423,761, exclusive of a trust fund of $5 million his father left him, which was reserved for his two daughters.

© Getty

© Getty1650: The Vanderbilt family first established roots in New York when Cornelius “the Commodore’s” great-great-great-grandfather Jan Aertson, a Dutch farmer, immigrated to what was then New Amsterdam as an indentured servant.

1794: The Commodore was born to a modest family on Staten Island, quitting school at the age of 11 to work on his father’s ferry. He decided to start his own ferry service when he was 16, borrowing $100 to purchase a periauger (a shallow-draft sailing vessel) to do so.

1867: He later expanded into steamboats, and eventually built his notoriously cutthroat railroad empire, New York Central, which he took control of in 1867, right before the Gilded Age boom. It boasted tracks across the Northeast and Midwest, and gave him a monopoly on all rail service in and out of New York City.

1877: Believing the bulk of the family fortune should be bestowed upon one descendant, he left his eldest son William Henry “Billy” Vanderbilt an 87% stake in New York Central. Billy subsequently expanded the business, reportedly doubling the family fortune to over $200 million.

1885: The following generations, however, weren’t so lucky — nor particularly pragmatic or productive. When Billy died, he split the family’s stake between both of his sons, Cornelius Vanderbilt II and William Kissam Vanderbilt, dividing the famed fortune.

1899: While both managed the railroads at one point, Cornelius II died in 1899, and William Kissam retired not long after. Moreover, their brother George Vanderbilt was already eating away at the fortune with his 146,000-acre Biltmore Estate in Asheville, North Carolina, which still stands today as America’s largest home.

1925: Anderson Cooper’s grandfather Reginald Claypoole Vanderbilt dies deeply in debt with a personal estate valued at $423,761.

Inheritance law during the reign of the Vanderbilt family

What was the legal context of this dramatic loss of wealth? “Trusts have for centuries been an effective tool for keeping wealth in a family line,” William LaPiana, Dean of Faculty at New York Law School and an expert on wills, trusts, and estates, tells HELLO!. However, he adds: “Before the end of the last century, making sure trusts lasted for more than about three generations required a lot of legal work, cooperation by younger generation family members, and a certain amount of luck.”

For many of the years that the Vanderbilt family was among the richest families in the US — if not the wealthiest — this Rule Against Perpetuities “was the law in more or less all of the states,” says LaPiana.

The common law, in place from the late 17th century until the late 20th, had “complex mechanisms” that limited the existence of a trust to about 100 years. “With the right planning and cooperative beneficiaries,” notes LaPiana, “new trusts could be created, and the cycle started all over again.”

© Getty Images

© Getty ImagesThe ‘Poor Little Rich Girl’ who built her own legacy

Then there was Cooper’s mother, “Poor Little Rich Girl,” Gloria Vanderbilt, who was born to Reginald and his spouse Gloria Morgan Vanderbilt in 1924. When Reginald died soon after, his young widow, who had married at 19, was just a month past her 21st birthday — and was charged with managing her infant daughter’s $2.5 million inheritance (about an estimated $47 million today).

Little Gloria earned her “Poor Little Rich Girl” nickname in 1934, when the then-ten-year-old was thrust into the center of a highly-publicized custody battle hailed as the “trial of the century.”

© Getty Images

© Getty Images“[My grandmother Gloria Morgan Vanderbilt] was spending a lot of what was essentially child support on her own care and feeding and social life.”

A family alliance launched the lawsuit against Gloria Morgan Vanderbilt: her mother, Laura Delphine Kilpatrick (nicknamed Naney Morgan), and little Gloria’s paternal aunt Gertrude Vanderbilt Whitney. The pair argued Gloria Morgan had all but disappeared from her daughter’s life, but was still collecting the $4,000 monthly payments she received from the little girl’s trust.

“[My grandmother Gloria Morgan Vanderbilt] was spending a lot of what was essentially child support on her own care and feeding and social life,” Cooper told Forbes in 2019. “Expenses piled up, and she was living lavishly on money that ultimately belonged to my mom.”

As a result, Aunt Gertrude won primary custody. From then on, young Gloria was only allowed to see her mother on weekends and certain holidays, typically accompanied by a detective and nurse. At the age of 21, Gloria received her trust fund of roughly $4.2 million; mother and daughter maintained an on-and-off relationship until Morgan Vanderbilt’s death in 1965.

© Getty Images

© Getty ImagesHow Gloria Vanderbilt earned her own millions in the 1970s

Gloria, who died at 95 in 2019, eventually became a woman of many hats; she was an artist, actress and author, among other roles, including, famously, a fashion designer.

Cooper’s mother is lauded as an early developer of designer blue jeans in the 1970s, launching her own line, which had her signature embroidered on the back pocket, with Indian designer Mohan Murjani’s Murjani Corporation in 1977.

The launch came with a million-dollar TV commercial campaign featuring Vanderbilt herself, and according to Murjani at the time, all 150,000 pairs of jeans the company produced sold out nearly instantly.

“Who has inherited a lot of money who has gone on to do things in their own life?”

Upon Gloria’s death in 2019, five years after Cooper’s comments on Howard Stern, documents obtained by Page Six revealed that he inherited the entirety of Gloria’s estate, which was estimated at less than $1.5 million, save for a Midtown East co-op at 30 Beekman Place, which went to her eldest child, Leopold “Stan” Stokowski, Cooper’s half-brother. (His late older brother, Carter Vanderbilt Cooper, died by suicide in 1988, when he was 23). Gloria’s middle child Christopher Stokowski, from whom she was estranged, received nothing.

Cooper noted that his mom — who he said was an “anomaly” in having made “more money in her own life than she ever inherited” despite her infamous trust fund — told him there was “none of that” when it came to a trust fund of his own.

© Getty Images

© Getty ImagesModern trusts: An expert weighs in

Cooper himself, of course, has meanwhile amassed his own fortune, and gained a pair of potential inheritors in his two young sons. Though details aren’t nearly as publicly disclosed as his ancestor’s financials used to be, Cooper, who in May 2026 left 60 Minutes after nearly 20 years as a correspondent, still anchors CNN’s prime-time news program Anderson Cooper 360°, among other ventures. He is reportedly paid $18 million a year by CNN, according to veteran media journalist Dylan Byers.

Appearing on a 2021 episode of Air Mail’s the Morning Meeting podcast, the news icon again declared he has no intention of leaving his then one-year-old son Wyatt (Sebastian was born in 2022) an inheritance when he dies, reiterating: “I don’t believe in passing on huge amounts of money. I don’t know what I’ll have,” and maintaining: “I’m not that interested in money, but I don’t intend to have some sort of pot of gold for my son. I’ll go with what my parents said… ‘College will be paid for, and then you gotta get on it.'”

The father-of-two might still be wary about how much he leaves to his own family, but his ancestors’ financial fate need not be his own. After all, not all trusts are created equal. “The wealthiest families today use a variety of structures, including trusts, LLCs, family partnerships, and other entities, to both accomplish tax planning and to preserve wealth,” notes trust expert LaPiana. “Often the wealthiest have private trust companies devoted to managing the family portfolio.”

“The alternative to planning that includes trusts is to give people outright ownership of property and let them in effect sink or swim.”

LaPiana also outlines a key factor in modern trusts, which might have Cooper perking up his ears. “Perhaps the most important development in the attempt to prevent the existence of a trust from diminishing the beneficiaries’ ambition is to tie distributions from the trust to certain benchmarks,” LaPiana suggests. This might mean a beneficiary will only receive distributions if they earn a bachelor’s degree or have a paying job. Some could even require an heir to pass a drug test.

“Trusts including these sorts of requirements are often called ‘incentive trusts,'” says the expert. Although it is difficult to know just how many such trusts exist, he adds that discussion within the profession indicates incentive trusts are far more common than they were some 20 years ago.

© Instagram

© Instagram“The alternative to planning that includes trusts is to give people outright ownership of property and let them in effect sink or swim, manage it prudently and carefully, or squander it – either through uncontrolled spending or bad choices in investments,” LaPiana reminds us.

He acknowledges: “In the end, there is a tension between wanting children and more remote descendants to be responsible adults — a condition I think our society equates in part with earning one’s own living — and protecting them from scams and bad judgment, especially with regard to managing wealth.”

Cooper undoubtedly has far more tools today than his grandfather, or even his mother, had to manage his wealth, and yes, there’s that potential inheritance to consider. “Very large fortunes probably have to be professionally managed, and there is [an] entire industry devoted to doing so,” concludes LaPiana.

Read the full article here